Retiring in Canada with $500,000 is possible, but the outcome depends strongly on variables like homeownership, pension access, investment returns, and government benefits timing choices.

Overview: The Retirement Scenario

Mitt and Kit Schmidt, a couple turning 65 from Stoner, BC, are the main case study. They have a combined $400,000 in RRSPs and $100,000 in TFSAs, totaling $500,000, plus a debt-free home valued at $600,000. Both qualify for full Old Age Security (OAS) and 75% of the max Canada Pension Plan (CPP) benefit from age 65. Their retirement income goals are:

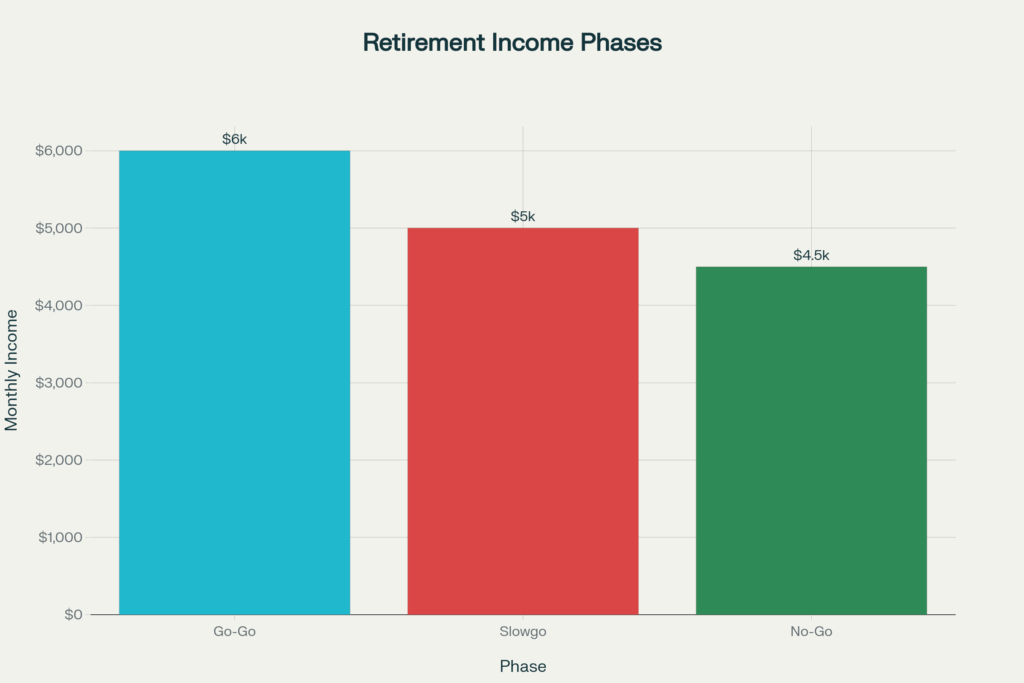

- Go-Go phase (65–74): $6,000/month after taxes

- Slowgo phase (75–84): $5,000/month after taxes

- No-Go phase (85+): $4,500/month after taxes

Assumptions include 3% inflation, a 5% post-fee annual investment return, and a planned lifespan to age 90.

Income Phases Chart

Monthly income goals shift over time, reflecting the realities of aging and lowered spending needs:

Monthly Retirement Income Phases for Mitt and Kit

Investment Approach and Initial Projections

- With no emergency fund included (though strongly recommended as critical), the base scenario rates Mitt and Kit at 95% “solve”—meaning their plan nearly meets their income needs until end-of-life.

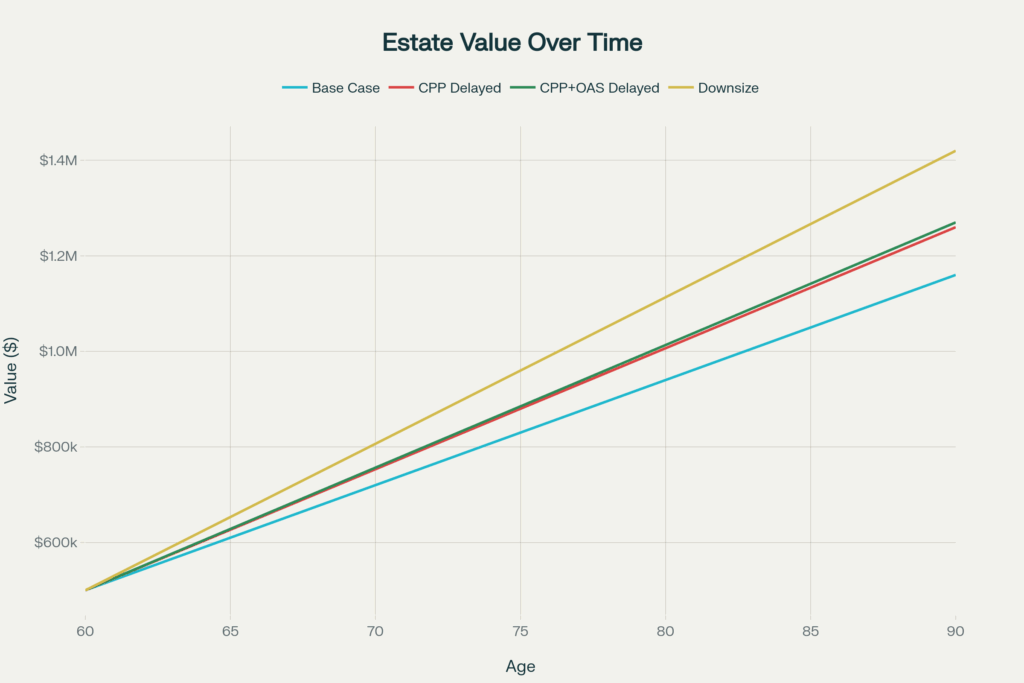

- Their projected estate value at death (age 90) is $1.16 million, mostly tied up in their home.

Inflation means rising annual income needs, visible in bar charts for each retirement year. By age 87, their spendable investments are projected to run out, leaving only government benefits and their home as assets, with a cash flow shortfall for the last 4 years.

Fundamental Retirement Levers Examined

Key variables can make a decisive difference:

- Delaying CPP to Age 70:

- Boosts plan strength to 99% solve, raises annual CPP payout by 42%, and lifts estate value by $99,000.

- Provides higher guaranteed, inflation-indexed income for late life, though means drawing down investments earlier.

- Delaying Both CPP and OAS to Age 70:

- Makes the plan fully funded (100% solve), but delaying OAS is less attractive due to lack of survivor benefit—income disappears if one spouse dies early.

- Adjusting TFSA Withdrawals:

- Holding off on TFSA withdrawals until needed lumpsum expenses or later years is preferable, maximizing tax-free compounding. This brings the plan back up to 100% on track.

Portfolio Risk and Spending Adjustments

- Switching to a Growth Portfolio (6%):

- Raises the plan’s solve rate by 4%, translating to 7 more years of retirement income, but comes with increased market volatility.

- Reducing Monthly Spending:

- Cutting $300/month (a 5% decrease) boosts plan surplus to 107%, but the couple found such lifestyle cuts unpalatable.

- Supplemental Income:

- Part-time work earning $15,000/year for 5 years increases solve rate to 106%—a practical buffer.

- Downsizing Their Home:

- Selling the home after 10 years for $600K, buying a $400K condo, and adding the $200K surplus to investments spikes their solve rate to 123%, giving extraordinary buffer for adverse events.

Stress Testing for Bumps in the Road

Scenarios with higher inflation (4%), lower returns (4%), and a 40% market crash soon after retiring were stress-tested:

- This disaster scenario drops solve rate back to 94%—about where the plan started. Reducing spending by 10% could bring the plan back into balance.

- Key lesson: Resilience comes from flexibility—adjusting spending, delaying benefits, or using home equity if needed.

Additional Scenarios: Pensions, Housing, Singles

- Defined Benefit Pension:

- Adding even a modest $1,000/month inflation-indexed pension at age 65 lifts solve rate to 110%, with room to boost lifestyle or leave a larger estate.

- No Homeownership:

- Losing the home only affects estate value, not initial retirement income solve rate. Alternative strategies like delaying CPP, working longer, and careful spending adjustment can keep solve rate above 100%, but end-of-life estate value drops to near zero.

- Income and Estate Value Chart

This chart illustrates how different strategies affect Mitt and Kit’s estate at age 90:

Estate Value at Age 90 under Different Strategies

Single Retiree Scenario

For singles, the numbers change dramatically:

- Hannah, age 65, with identical assets but only one set of CPP and OAS, starts at 54% solve rate.

- Adjusting monthly spending—Go-Go ($4,500), Slowgo ($4,000), No-go ($3,500)—climbs up to 77% solve.

- Delaying CPP to 70, careful TFSA/RRSP management, working an extra year before retirement, and earning $20,000 in part-time income for 5 years pushes the solve rate near 99%.

- Many expenses—housing, internet, heating—don’t drop much for singles, so plan flexibility is essential.

Key Takeaways and Planning Wisdom

- Retirement success on $500,000 depends on a combination of factors—pension, homeownership, investing strategy, government program timing, supplemental income, and spending flexibility.

- Stress-testing for market shocks and inflation is crucial. Flexibility—working longer, spending less, or tapping assets—builds resilience.

- Defined benefit pensions and downsizing property can make enormous positive impacts.

- Singles must plan for bigger shortfalls and consider earning longer, delaying benefits, or sharply controlling expenses.

- Careful withdrawal planning (especially on TFSAs and RRSPs to manage tax and compound growth) pays off.

- Using robust retirement planning software and consulting with a professional are strongly recommended for individualized strategies.